GPU Providers & Data Centers

Anchor your pricing strategy to market expectations. Benchmark rental rates against the term structure, identify contango or backwardation regimes, and structure long-term contracts with market-calibrated confidence.

Forward Curve

See where GPU rental prices are heading — not just where they are. Term-structure rates and no-arbitrage forward pricing up to 36 months horizon.

TARGET SEGMENT USE CASES

Anchor your pricing strategy to market expectations. Benchmark rental rates against the term structure, identify contango or backwardation regimes, and structure long-term contracts with market-calibrated confidence.

Time your procurement. Compare locked-in term rates against forward expectations to decide when to commit, when to wait, and when to negotiate. Validate every broker quote against the curve.

The no-arbitrage forward rate is your settlement reference. Price swaps, build structured products, underwrite GPU-collateralized loans, and design parametric insurance — all anchored to a published, methodology-backed forward curve.

METHODOLOGY & DATA SCHEMA

We collect actual GPU rental transaction data and published rates across 95% of Neo-Cloud providers and 100% of major hyperscalers.

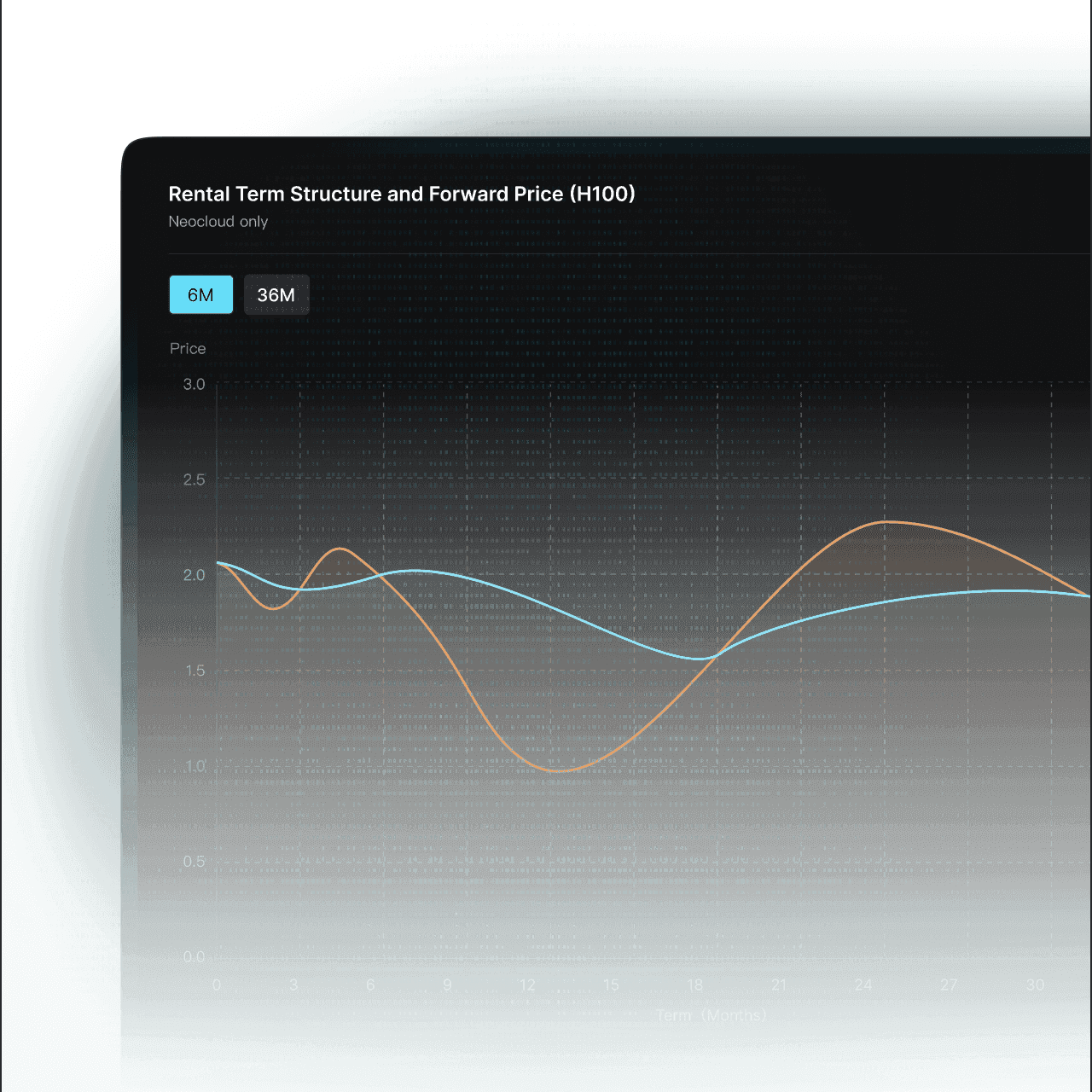

Rental rates are organized by term length (1-month through 36-month) to build the term structure (the blue line).

The forward rate (orange line) is mathematically derived from the term structure using established no-arbitrage pricing methodology.

Both curves are recalculated every business day and can be accessed via the Silicon Data portal.

FORWARD CURVE

The Term Structure Rate (the blue line) represents the actual cost you would pay today to lock in a GPU rental for a specific duration (e.g., a 12-month contract). The Forward Rate (the orange line) is a mathematical derivation that shows the market's expected spot rental price at a specific point in the future (e.g., what a 1-month rental will cost exactly 12 months from now).

The Forward Curve currently tracks the Nvidia H100, B200 and A100 markets, as these possess the trading volume and liquidity required for robust forward pricing. Forward indices for other GPU models will be published as those markets mature.

Yes. Unlike static pricing aggregators, the Silicon Data Forward Curve is built specifically for financial application. By utilizing standard no-arbitrage derivation and publishing daily, the curve serves as a reliable, methodology-backed reference rate for pricing and settling compute futures, swaps, options, and parametric insurance products.

Depending on your subscription tier, the Forward Curve data is accessible via direct REST API, the Silicon Data web portal, and directly through the Bloomberg Terminal (Ticker: SDH100RT).

Yes. Full historical data archives of the forward curve are available to users on our Enterprise Tier, enabling quant desks and researchers to backtest models and analyze historical contango/backwardation regimes.

The GPU Forward Curve delivers the term-structure rates and implied forward pricing that infrastructure operators need to plan — and that financial institutions need to build.