March 2026 RAM Price Update: DDR5 Spot Prices Dip While GDDR6 Stays Firm

DDR5 chip spot prices softened after the TurboQuant announcement while GDDR6 kept rising.

Silicon Data | March 31, 2026

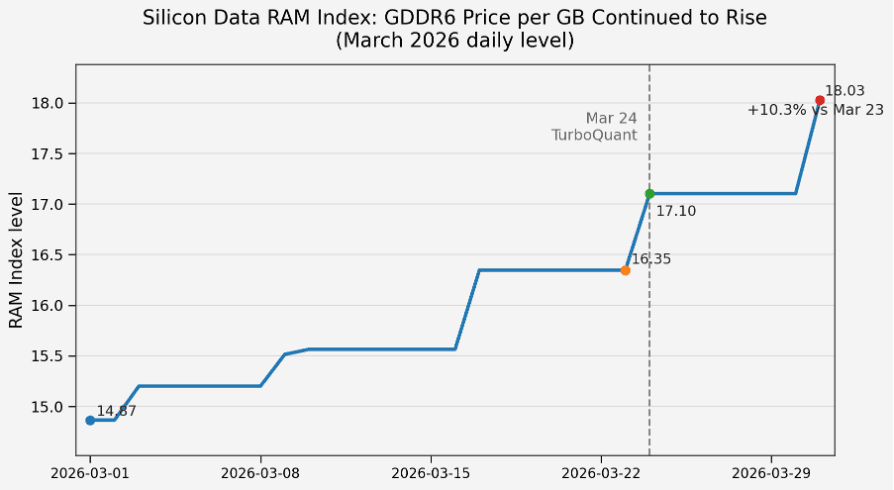

The late-March selloff in memory stocks looked broad, but the pricing signal underneath was not. In Silicon Data's March sample, DDR5 chip spot pricing softened modestly after the TurboQuant shock, while GDDR6 kept moving higher. The RAM Index adds an even cleaner confirmation: Silicon Data's proprietary GDDR6 price-per-GB tracker rose from 16.35 on Mar. 23 to 18.03 on Mar. 31, even as memory equities sold off after the TurboQuant headlines. The gap between equity reaction and product pricing is the core story.

What the Silicon Data sample shows

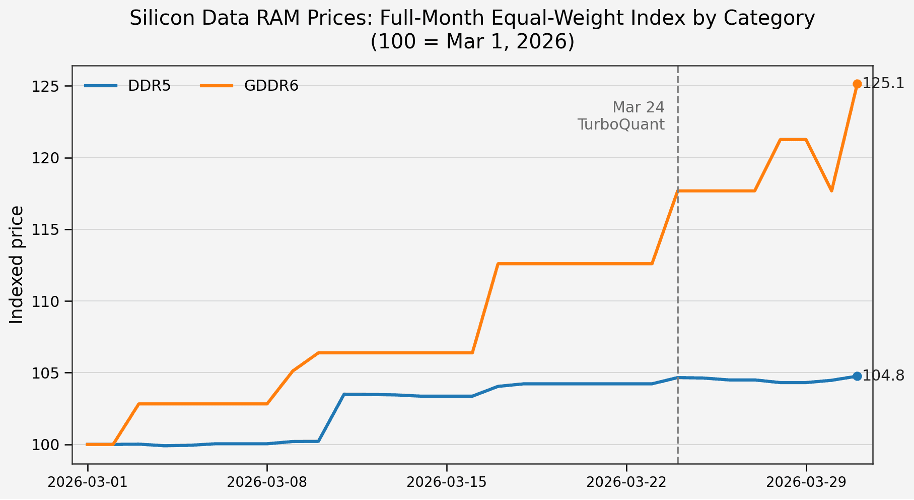

The March file covers 21 tracked RAM products: 4 DDR5 chip spot SKUs, 15 DDR5 module SKUs, and 2 GDDR6 chip spot SKUs. After averaging same-day quotes at the SKU level and indexing Mar. 1 to 100, the DDR5 category ended the month at 104.8, while GDDR6 reached 125.1. Because Figure 1 is a category-level view that includes both DDR5 chips and modules, DDR5 can still finish the month up versus Mar. 1 even if chip-only pricing softened later in March.

Figure 1. In Silicon Data's full sample, DDR5 finished modestly above Mar. 1, while GDDR6 kept moving higher.

Why DDR5 softened

TurboQuant gave investors a concrete reason to question how much premium memory the AI stack will need per unit of inference. Google Research said TurboQuant can quantize the LLM key-value cache to 3 bits without retraining or fine-tuning, while cutting KV-cache memory usage by at least 6x. Because KV cache is an inference-side memory bottleneck, that was enough to pressure memory equities quickly.

The market reaction was immediate. U.S. and Korean memory names sold off sharply after the announcement, which helped pull down sentiment around AI-linked DRAM exposure. TrendForce's late-March DRAM update also showed why DDR5 was vulnerable: March contract pricing was flat while spot prices were already trading above contract, leaving spot momentum easier to disrupt.

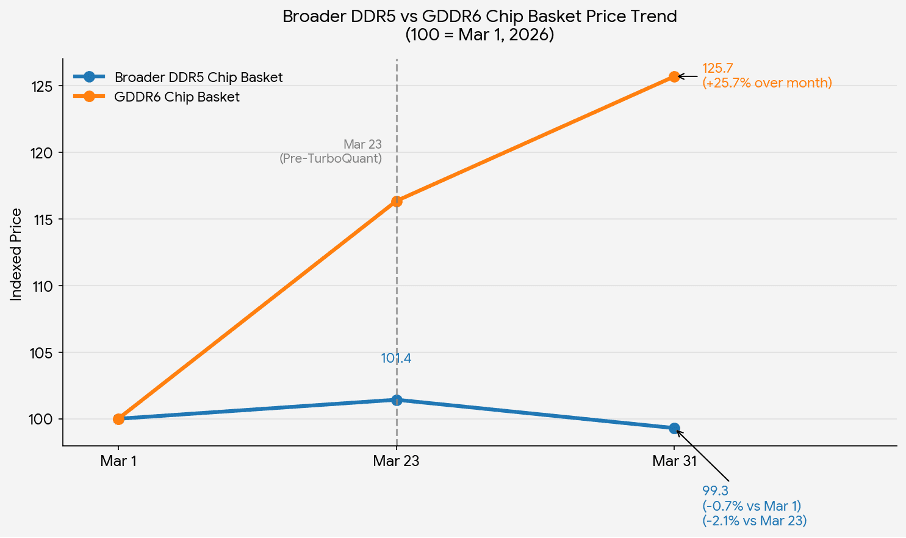

Figure 2. The broader DDR5 chip basket finished almost flat versus Mar. 1, while the GDDR6 chip basket rose significantly over the month.

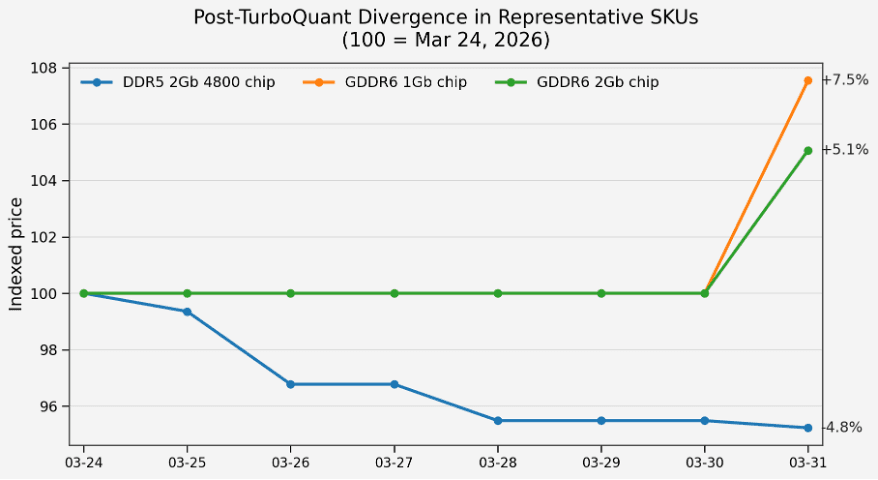

That distinction matters for reading the charts. Figure 3 zooms in on representative chip spot pricing after Mar. 24: the DDR5 2Gb 4800 chip ended Mar. 31 down 4.8% from Mar. 24, while the GDDR6 1Gb and 2Gb chips finished up 7.5% and 5.1%. The broader DDR5 chip basket tells the same directional story (Figure 2): it finished almost flat versus Mar. 1 (-0.7%) and modestly lower from Mar. 23 (-2.1%), while the GDDR6 chip basket rose +25.7% over the month. In other words, the late-March shock hit AI-linked DDR5 pricing more than graphics-memory pricing.

Figure 3. Relative to Mar. 24, a representative DDR5 chip moved lower while GDDR6 SKUs stayed firm to higher.

Why GDDR6 stayed firm

First, the demand exposure is different. TurboQuant compresses inference-side KV cache; it does not directly reduce gaming graphics-memory demand. That matters because GDDR6 still sits mainly in gaming GPUs and consoles. AMD's Radeon RX 9070 uses GDDR6, and both PlayStation 5 and Xbox Series X list 16 GB of GDDR6 memory.

Second, specialty-memory supply is still tight. TrendForce has said AI-equivalent demand could absorb nearly 20% of global DRAM output in 2026, while meaningful new DRAM capacity is unlikely before 2027. (That same supply tightness is one of the factors behind rising GPU rental prices heading into 2026.) When supply is scarce, vendors rationally prioritize the highest-value memory categories, which keeps graphics-memory pricing firmer than a headline-driven equity move might suggest.

Third, pricing is stickier. Reuters reported in March that Samsung is pushing major customers toward three-to-five-year chip agreements. That does not prove every GDDR6 deal is locked, but it is consistent with slower price transmission than in retail DDR5 modules. TrendForce also reported that rising GDDR6 and GDDR7 costs were already feeding planned GPU price increases, which implies downstream customers were still absorbing higher graphics-memory costs rather than forcing an immediate reversal.

What RAM Index adds

RAM Index is Silicon Data's proprietary tracker of GDDR6 price per GB. It matters because a handful of chip quotes can show direction, but a dedicated price-per-GB series is a cleaner way to monitor graphics-memory inflation over time.

In March, the RAM Index rose from 14.87 on Mar. 1 to 18.03 on Mar. 31 (+21.3%). More important for this debate, it rose from 16.35 on Mar. 23 to 18.03 on Mar. 31 (+10.3%), and from 17.10 on Mar. 24 to 18.03 on Mar. 31 (+5.4%). That is the opposite of a post-TurboQuant GDDR6 price unwind.

Because RAM Index tracks GDDR6 in price-per-GB terms, it strips away some of the noise created by SKU mix and packaging differences. It therefore strengthens the central conclusion: late-March weakness in memory stocks reflected a re-rating of AI and HBM expectations, not a broad-based collapse in graphics-memory pricing.

Figure 4. Silicon Data RAM Index - a proprietary GDDR6 price-per-GB tracker - kept rising through month-end.

Bottom line

The late-March selloff was a narrative shock, not a synchronized collapse across every RAM category. In Silicon Data, DDR5 chip spot prices blinked, but GDDR6 stayed firm - and RAM Index makes that even clearer. The cleanest read is that TurboQuant pressured expectations for AI-memory intensity, while GDDR6 remained anchored by gaming and console demand, tight specialty-memory supply, and stickier pricing mechanics.

Frequently Asked Questions

RAM Index is Silicon Data's proprietary tracker of GDDR6 price per GB. A dedicated price-per-GB series gives a cleaner read on graphics-memory inflation than a handful of individual chip quotes — in March 2026 it rose from 14.87 on Mar. 1 to 18.03 on Mar. 31 (+21.3%).

DDR5 chip spot pricing softened modestly after the TurboQuant shock — a representative DDR5 2Gb 4800 chip ended Mar. 31 down 4.8% from Mar. 24, and the broader DDR5 chip basket finished roughly flat versus Mar. 1 (−0.7%). Category-level DDR5 (chips plus modules) still closed the month up at 104.8 vs. 100 on Mar. 1.

GDDR6 demand is tied to gaming GPUs and consoles, which TurboQuant's inference-side KV-cache compression does not reduce; specialty-memory supply stays tight (AI could absorb ~20% of 2026 DRAM output, with little new capacity before 2027); and GDDR6 pricing is stickier. The GDDR6 chip basket rose +25.7% over the month.

TurboQuant is a Google Research method that quantizes the LLM key-value cache to 3 bits without retraining or fine-tuning, cutting KV-cache memory usage by at least 6×. Because KV cache is an inference-side memory bottleneck, it pressured AI-linked memory equities and DDR5 sentiment quickly — a narrative shock rather than a broad pricing collapse.

Through Silicon Data's products — the RAM Index for GDDR6 price-per-GB and SiliconNavigator for daily GPU rental pricing across chipsets, regions, and rental terms — all available via API.