May 2026 RAM Price Update: GDDR6 Unwinds the March Spike While DDR5 Grinds Higher

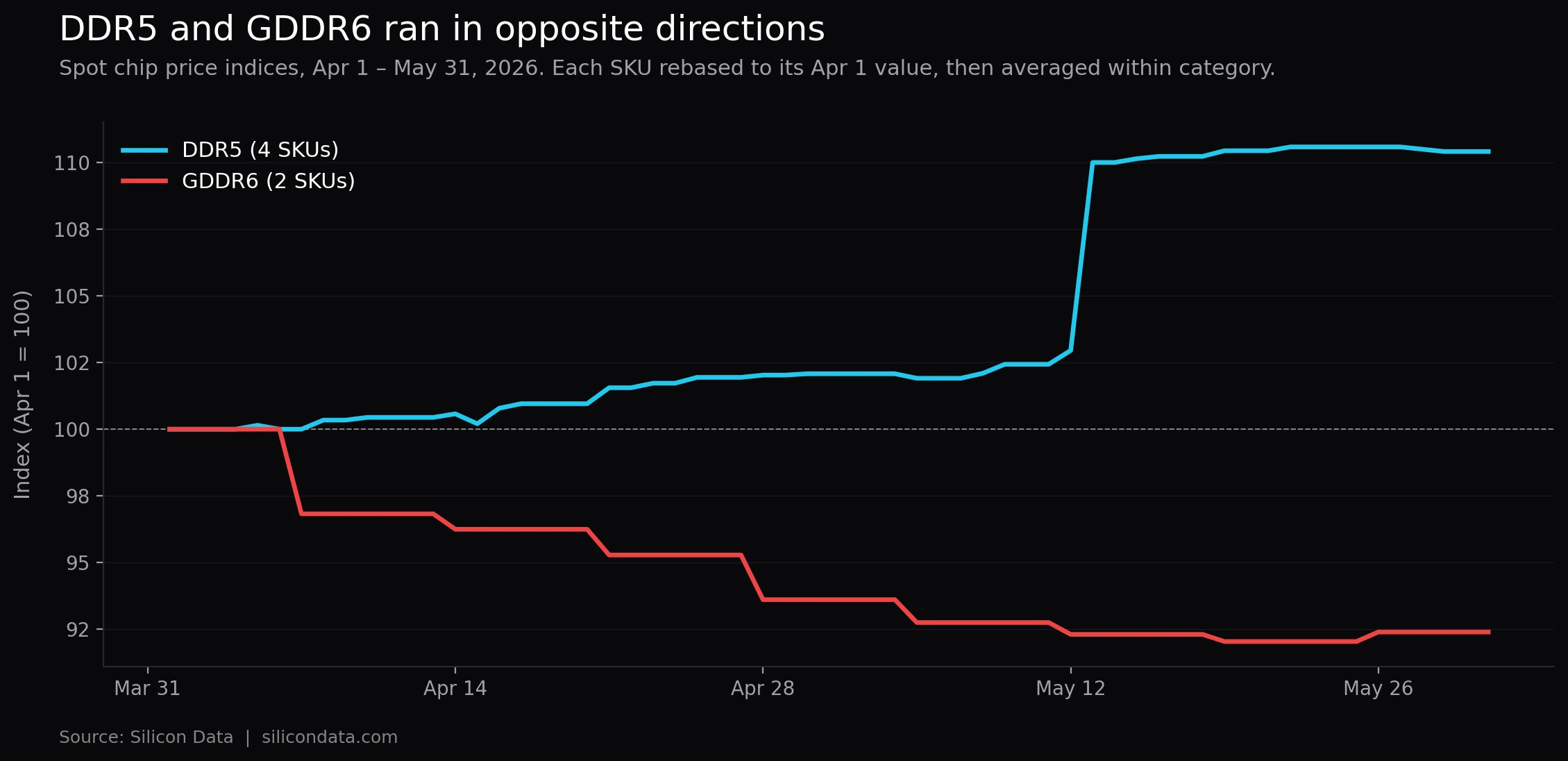

GDDR6 spot prices unwound the March spike while DDR5 chips stepped up sharply on May 13. Silicon Data RAM Index and SKU data.

The late-March GDDR6 rally turned out to be the local top. Across April and May, GDDR6 spot prices drifted lower while DDR5 chip prices ground higher — and the higher-density DDR5 SKUs took a single-day step up on May 13. The post-TurboQuant memory selloff did not kill AI-memory demand. It just rotated where the strength was sitting.

What changed since March

The March update ended with GDDR6 firmly bid (RAM Index at 18.03 on Mar. 31) and DDR5 chip pricing softening at the margins after the TurboQuant headline. April and May reversed that pattern in the broader DRAM market. In Silicon Data's sample of six tracked SKUs (four DDR5 chip SKUs, two GDDR6 chip SKUs), every DDR5 SKU finished higher across the window, every GDDR6 SKU finished lower, and the size of the moves was material.

| SKU | Apr 1 | May 31 | Change |

|---|---|---|---|

| DDR5 16Gb (2Gx8) 4800/5600 | $18.45 | $20.65 | +11.9% |

| DDR5 16Gb Major | $15.00 | $17.50 | +16.7% |

| DDR5 24Gb Major | $12.00 | $13.33 | +11.1% |

| DDR5 16Gb eTT | $11.23 | $11.45 | +1.9% |

| GDDR6 8Gb | $12.87 | $11.63 | −9.6% |

| GDDR6 16Gb | $19.32 | $18.23 | −5.6% |

Indexed to Apr 1 = 100, the DDR5 category ended May at 110.4. The GDDR6 category ended at 92.4. That is an 18-point spread that opened up in eight weeks.

The RAM Index tells a clean version of the GDDR6 story

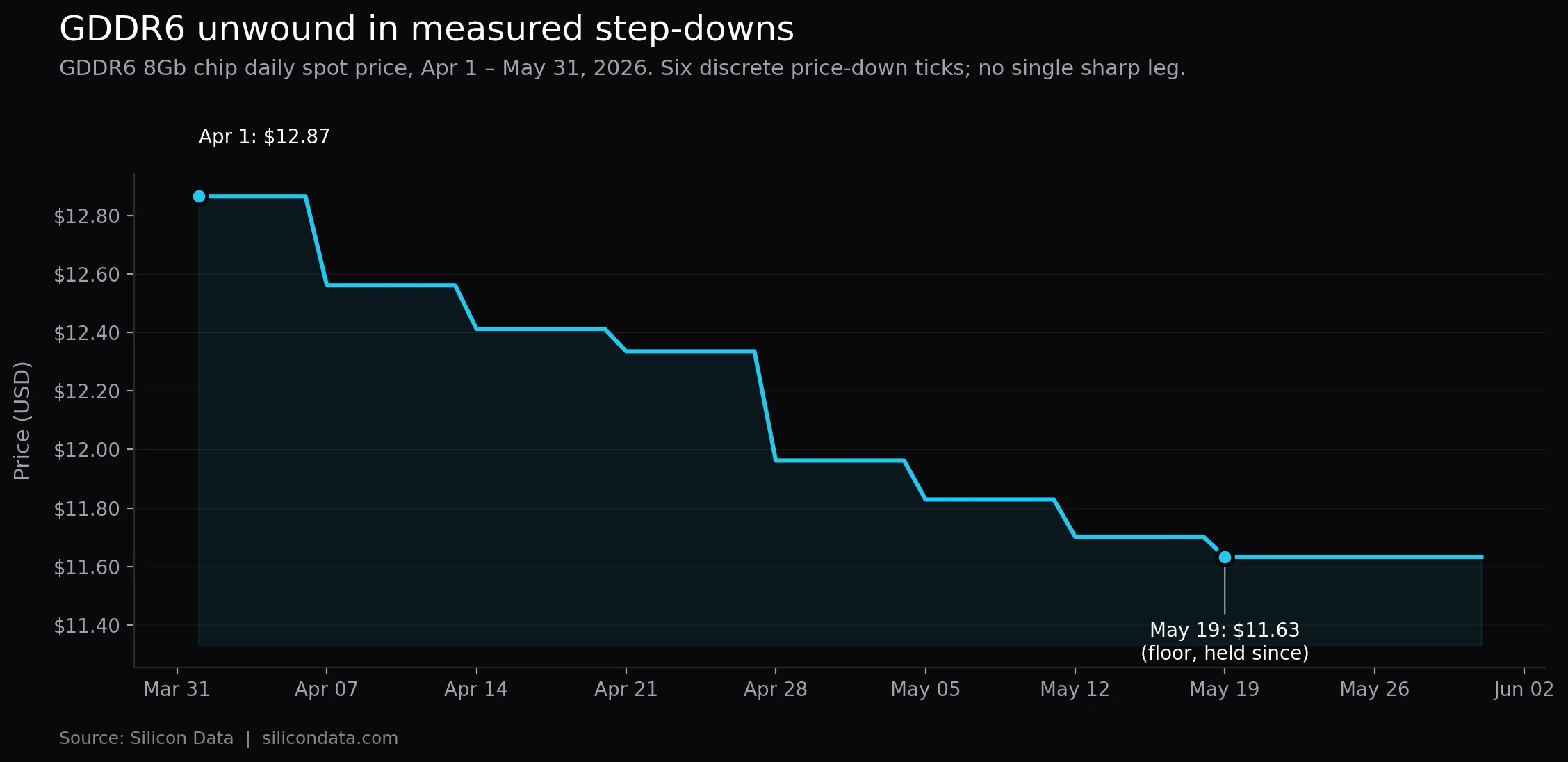

RAM Index — Silicon Data's GDDR6 price-per-gigabyte tracker — peaked at 18.03 on Mar. 31 and has been grinding lower since. By May 24 the Index was at 16.80, down 6.8% from the March peak. It has begun to stabilize in early June, ticking up to 16.99 on Jun. 8, but the broader move from late March through May was a measured unwind, not a sharp break.

The shape of the move matters as much as the magnitude. RAM Index did not collapse — it drifted, in a series of small step-downs spaced several days apart, with no single sharp leg. That is consistent with what specialty-memory price unwinds typically look like when the underlying inventory and order-book are still relatively tight: vendors give back the margin gradually rather than all at once, and contract pricing buffers the spot move.

The per-chip detail tells the same story in finer grain. The GDDR6 8Gb chip moved through six discrete price-down ticks from Apr. 1 ($12.87) to May 19 ($11.63), where it has held. The GDDR6 16Gb chip followed an even more compressed trajectory — five small step-downs from $19.32 on Apr. 1 to $18.08 on May 5, then a small reflexive uptick to $18.23 in late May. Both SKUs show the same pattern: persistent downward pressure through April and early May, stabilizing in the second half of May.

DDR5 ran the opposite direction — and jumped on May 13

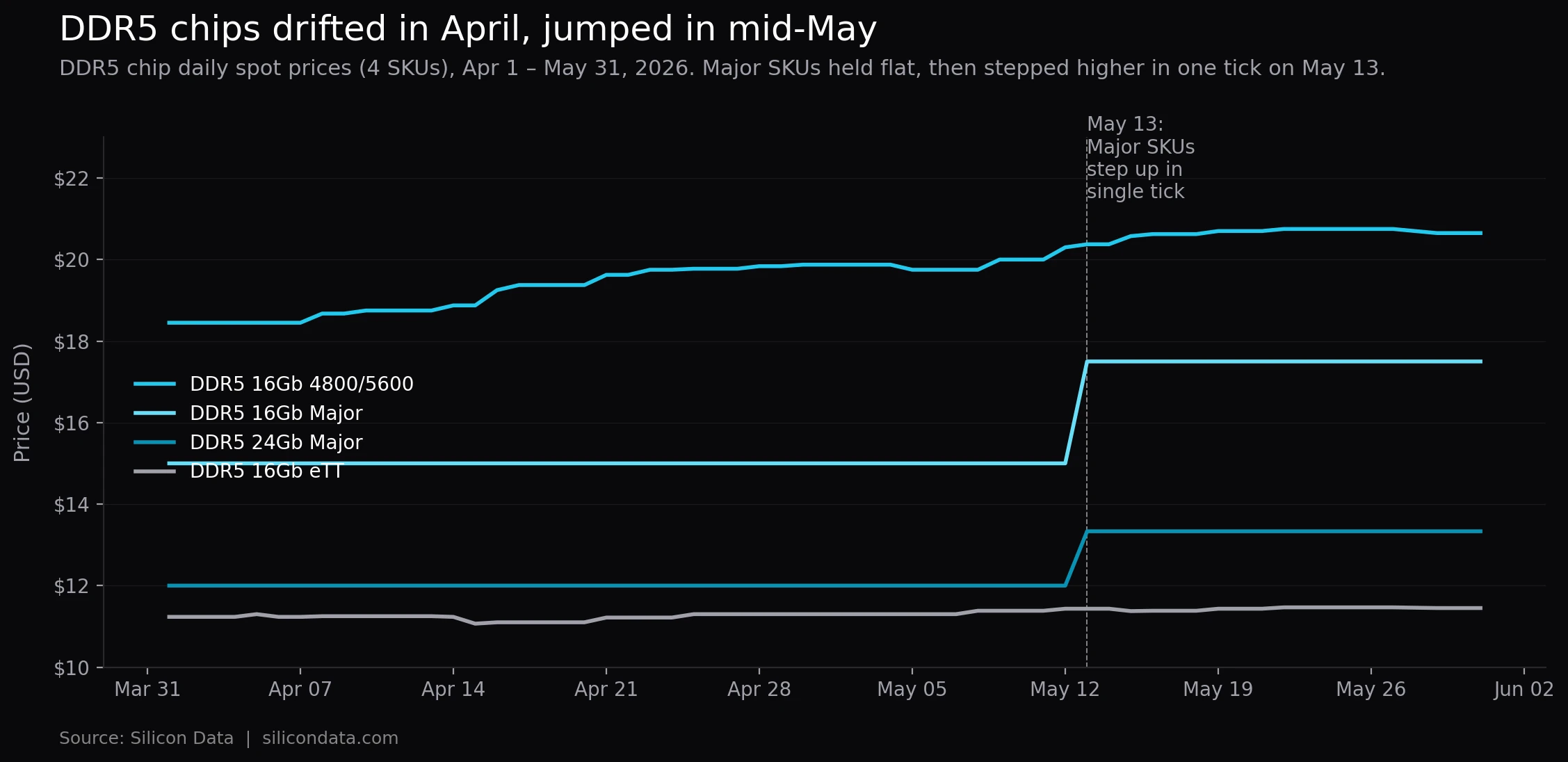

DDR5 chip prices were quiet in April. The DDR5 16Gb 4800/5600 SKU drifted from $18.45 on Apr. 1 to $19.88 by Apr. 30 — a steady +7.7% climb spread across the whole month. The two "Major" SKUs (DDR5 16Gb at $15.00 and DDR5 24Gb at $12.00) were unchanged through all of April and the first twelve days of May.

May 13 is when the regime broke. Both Major SKUs jumped in a single day with no warm-up: DDR5 16Gb Major from $15.00 to $17.50 (+16.7%), DDR5 24Gb Major from $12.00 to $13.33 (+11.1%). Both then held flat at the new level for the rest of May. The 4800/5600 SKU added another 3.9% on top of its April rise across the same window.

A single-day step of this size is more consistent with a discrete repricing event — a vendor list-price reset, or a contract-cycle reset where spot reconverges to a newly higher contract reference — than with gradual demand pressure. The data shows the move and that the new level held through the rest of May; it does not identify the trigger.

The size of the daily moves differed by category. The DDR5 Major SKUs varied most over the window — a function of the single May 13 step — while the eTT SKU was nearly flat. GDDR6 prices moved in smaller increments because the decline was gradual rather than concentrated in one session.

Possible drivers of the rotation

The data shows GDDR6 declining and DDR5 rising over the same window; it does not establish why. A few mechanisms are consistent with the pattern, offered here as interpretation rather than conclusion.

The late-March GDDR6 rally may have carried an AI-adjacency premium alongside its gaming/console and supply-tightness support. If the TurboQuant news reduced expectations for memory intensity in inference workloads, the April–May drift is consistent with that premium gradually leaving the chip while the gaming and supply drivers stayed intact.

The DDR5 strength is concentrated in the higher-density Major SKUs rather than the commodity eTT tier. That is consistent with — though not proof of — server DDR5 demand, since those are the densities more likely to be specified into AI server builds. For context on how compute and memory pricing have moved this cycle, see Silicon Data's GPU Forward Curve and the B200 March update.

The May 13 step itself points more toward a contract-cycle reset than organic spot demand. TrendForce's late-March note flagged DDR5 spot trading above contract; a material upward contract reset in mid-May would produce the discrete spot move the data shows.

What the data does not yet show

The sample here is six SKUs of spot chip pricing — it does not include DDR5 modules, server contract pricing, or HBM. The DDR5 strength signal is suggestive, but a fuller read requires the module and contract layers, which are tracked separately through SiliconNavigator.

GDDR6's stabilization in late May is real but new. The May 19 floor at $11.63 on the 8Gb chip and the small May-26 uptick on the 16Gb chip together suggest the unwind is finding a level. Whether that holds depends on gaming and console demand into the back half of 2026 and on whether GDDR7 transition pricing pressure begins to show up in the GDDR6 spot market.

Bottom line

The March pattern — GDDR6 firm, DDR5 soft — reversed across April and May. GDDR6 declined in a measured unwind; DDR5 chip prices rose in April and stepped up sharply on May 13. One reading is that AI-memory demand did not weaken but shifted from GDDR6 toward higher-density DDR5; the data is consistent with that interpretation without confirming it.

The RAM Index tracks the GDDR6 side of this daily. Worth watching from here: whether the late-May stabilization in GDDR6 holds, and whether the post-May-13 DDR5 level is a new range or a one-off reset.

Frequently Asked Questions

The RAM Index is Silicon Data's proprietary daily tracker of GDDR6 price per gigabyte. It normalizes for SKU mix and packaging so the index moves on underlying price action rather than on changes in which products are quoted. As of Jun. 8, 2026, RAM Index stands at 16.99.

The late-March GDDR6 rally carried both a gaming/console demand premium and, plausibly, an AI-memory adjacency premium. The TurboQuant news appears to have reduced expectations for memory intensity in inference workloads without affecting the gaming or supply-tightness drivers. The April–May decline is consistent with that adjacency premium gradually unwinding, though the data does not confirm the cause.

Two DDR5 chip SKUs — the 16Gb Major and the 24Gb Major — stepped up in a single day after holding flat for six weeks. DDR5 16Gb Major went from $15.00 to $17.50 (+16.7%); DDR5 24Gb Major went from $12.00 to $13.33 (+11.1%). Both held at the new level through the rest of May. The discrete single-day pattern is more consistent with a contract-cycle reset or vendor list-price update than with gradual demand pressure.

It complements it. The March piece read the late-March selloff as a narrative shock that hit AI-linked DDR5 spot harder than gaming-linked GDDR6. April-May data shows that read was right for the day but the regime kept evolving: GDDR6 gave back the rally, and DDR5 — particularly the higher-density SKUs — caught a bid. Tracking month over month is how rotations like this become visible.

RAM Index publishes daily. Underlying SKU-level RAM and GPU pricing is tracked through SiliconNavigator. For methodology background on how Silicon Data constructs its index family, see Building a Robust GPU Index.